In the ever-shifting landscape of education finance, student loan interest rates stand as a pivotal force shaping the journeys of millions. As whispers of change grow louder, borrowers and policymakers alike find themselves navigating a new terrain-where the cost of borrowing could take unexpected turns. This article delves into the mechanics behind how student loan interest rates are set to change, unraveling the factors at play and what these shifts might mean for the future of funding higher education. Whether you’re a current student, a parent, or simply curious about the evolving world of student debt, understanding these changes is more important than ever.

Table of Contents

- Understanding the Current Landscape of Student Loan Interest Rates

- Factors Driving the Upcoming Changes in Interest Rates

- Impact of Interest Rate Adjustments on Borrowers’ Financial Planning

- Strategies to Manage Student Loans Amid Changing Interest Rates

- Expert Recommendations for Navigating Future Loan Repayments

- Frequently Asked Questions

- Wrapping Up

Understanding the Current Landscape of Student Loan Interest Rates

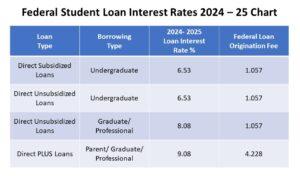

The student loan interest rate environment is anything but static. Over the past few years, rates have fluctuated due to economic shifts, government policy changes, and market conditions. Currently, interest rates are influenced by benchmark rates such as the U.S. Treasury yields, which serve as a base for federal student loan rates. This linkage means that when the economy experiences inflationary pressures or the Federal Reserve adjusts rates, student loan interest rates often follow suit.

In addition to market factors, government decisions play a crucial role. For instance, federal student loans have rates set annually based on the 10-year Treasury note auction in May, plus a fixed margin. This method ties student borrowing costs directly to the broader economic landscape, making it essential for borrowers to stay informed about federal budget plans and legislative proposals that might impact these rates.

Private student loans, however, operate under a different set of rules:

- Rates are determined by lenders based on the borrower’s creditworthiness and market competition.

- Variable rates can shift throughout the life of the loan, often tied to indexes like the prime rate.

- Fixed rates remain constant but may start higher than variable rates to compensate for lender risk.

| Loan Type | Rate Setting Method | Typical Rate Range (2024) |

|---|---|---|

| Federal Direct Subsidized | 10-year Treasury + fixed margin | 5.5% – 6.5% |

| Federal Direct Unsubsidized | 10-year Treasury + fixed margin | 5.5% – 6.5% |

| Private Loans | Credit-based, variable/fixed | 3.5% – 14% |

Factors Driving the Upcoming Changes in Interest Rates

Several critical elements are converging to influence the trajectory of student loan interest rates in the near future. At the forefront is the macro-economic environment, particularly inflation trends and Federal Reserve policies. As inflation pressures persist, the central bank may opt to adjust benchmark rates, indirectly nudging student loan interest rates higher or lower depending on their economic outlook.

Another pivotal factor is the government’s fiscal stance. Legislative decisions regarding student debt relief, budget allocations, and funding for educational programs can significantly impact how interest rates are structured. For instance, increased funding for subsidized loans or targeted relief programs could result in more favorable rates for borrowers.

Technological advancements and data analytics are also playing a surprising role. Enhanced risk assessment models allow lenders to tailor interest rates more precisely, reflecting individual borrower profiles rather than broad categorizations. This shift could lead to a more dynamic and personalized rate-setting mechanism.

- Inflation and Federal Reserve policy: Direct impact on base rates.

- Government budget priorities: Influence on loan subsidies and relief.

- Advances in risk modeling: Personalized interest rate adjustments.

| Factor | Potential Impact | Timeframe |

|---|---|---|

| Inflation Rates | Increase in interest rates | Short to Medium Term |

| Federal Budget Policy | Possible rate relief or hikes | Medium Term |

| Risk Assessment Tech | More personalized rates | Long Term |

Impact of Interest Rate Adjustments on Borrowers’ Financial Planning

Adjustments in student loan interest rates ripple through borrowers’ financial landscapes, often prompting a reassessment of budgets and long-term goals. When rates rise, monthly payments typically increase, potentially stretching already tight finances. Conversely, rate reductions can offer some breathing room, allowing borrowers to accelerate repayments or divert funds toward other priorities like savings or investments.

Effective financial planning amid fluctuating interest rates demands flexibility and foresight. Borrowers may find it beneficial to:

- Reevaluate repayment strategies: Shifting from standard to graduated plans or exploring income-driven options can align payments better with current income levels.

- Consider refinancing: Locking in a lower fixed rate might protect against future hikes, though eligibility and terms vary.

- Build emergency reserves: Cushioning against unexpected expenses is critical, especially when payment amounts are unpredictable.

Below is a simplified comparison showing how different interest rate scenarios can impact a $30,000 student loan over a 10-year repayment period:

| Interest Rate | Estimated Monthly Payment | Total Interest Paid |

|---|---|---|

| 4.5% | $310 | $7,720 |

| 6.0% | $333 | $9,960 |

| 7.5% | $355 | $12,600 |

Ultimately, staying informed and proactive in response to interest rate changes empowers borrowers to maintain control over their financial journeys, minimizing stress and maximizing the potential for successful repayment.

Strategies to Manage Student Loans Amid Changing Interest Rates

When interest rates fluctuate, students and graduates face an evolving landscape that can significantly impact loan repayment plans. One effective approach is to refinance or consolidate loans when rates drop, potentially locking in a lower rate to reduce overall interest payments. This strategy, however, requires careful analysis of current loan terms, as refinancing federal loans into private loans may result in losing certain borrower protections.

Another key tactic involves adjusting payment schedules to align with personal financial situations and anticipated rate changes. For example, increasing monthly payments during periods of low interest can help pay down principal faster, minimizing the impact of future rate hikes. Conversely, opting for income-driven repayment plans can provide flexibility if rates rise and monthly payments become less affordable.

Staying informed about policy shifts and market trends is crucial. Utilizing online calculators and borrower tools can assist in projecting how different interest rate scenarios affect total repayment. Below is a quick comparison of common strategies and their potential benefits:

| Strategy | Best Use Case | Potential Benefit |

|---|---|---|

| Loan Refinancing | When rates drop significantly | Lower monthly payments & interest |

| Income-Driven Repayment | Fluctuating income & rising rates | Payment flexibility |

| Extra Principal Payments | Stable finances & low rates | Faster loan payoff |

| Loan Consolidation | Multiple loans with varying rates | Simplified payments |

- Review loan terms regularly to identify opportunities for refinancing or consolidation.

- Maintain an emergency fund to avoid missed payments during rate increases.

- Consult financial advisors to tailor strategies based on individual circumstances.

Expert Recommendations for Navigating Future Loan Repayments

When facing shifting interest rates, the key to managing your student loans effectively lies in proactive planning and strategic decision-making. Experts stress the importance of regularly reviewing your loan terms and staying informed about federal announcements. This allows borrowers to anticipate changes and adjust their repayment strategies accordingly, avoiding surprises down the road.

One practical approach is to consider refinancing options if your current loans carry variable rates that may escalate. Refinancing can lock in a fixed interest rate, potentially saving thousands over the life of the loan. However, it’s crucial to weigh the benefits against any possible loss of federal loan protections.

Financial advisors also recommend building a flexible repayment plan that can adapt to rate fluctuations. This might involve:

- Setting aside a buffer fund for unexpected increases

- Exploring income-driven repayment plans that adjust based on your earnings

- Making extra payments toward principal whenever possible

Below is a simple comparison table to help you visualize how different repayment strategies might impact your total interest paid over a 10-year period:

| Repayment Strategy | Estimated Interest Over 10 Years | Pros | Cons |

|---|---|---|---|

| Standard Fixed Rate | $8,500 | Predictable payments | Less flexibility |

| Variable Rate | $7,200 – $10,000 | Potential savings if rates stay low | Risk of higher payments |

| Income-Driven Plan | $6,000 – $9,000 | Payments based on income | Longer repayment term |

Frequently Asked Questions

Q&A: How Student Loan Interest Rates Are Set to Change

Q1: What’s driving the change in student loan interest rates?

A1: The shift in student loan interest rates is largely influenced by broader economic factors such as inflation, government monetary policy, and decisions made by financial regulators. Changes in the federal funds rate and Treasury bond yields often ripple into loan rates, prompting adjustments to keep pace with the economic climate.

Q2: How exactly do student loan interest rates get determined?

A2: For federal student loans, interest rates are typically set each year based on the yield of 10-year Treasury notes plus a fixed margin established by Congress. Private student loans, meanwhile, rely on lenders’ assessments of market conditions, borrower creditworthiness, and competitive factors, which means their rates can be more variable.

Q3: When will these new interest rates take effect?

A3: Federal student loan interest rates reset annually on July 1st for new loans disbursed in the upcoming academic year. Private lenders may adjust rates at various times throughout the year, often aligning with changes in benchmark rates like the prime rate or LIBOR replacement rates.

Q4: Will these changes affect current borrowers or only new loans?

A4: Generally, interest rates on existing federal student loans are fixed once the loan is disbursed, so current borrowers won’t see their rates change retroactively. New loans, however, will reflect the updated rates. Private loans may have variable rates, so some current borrowers could experience changes depending on their loan terms.

Q5: What impact might these changes have on students and graduates?

A5: Rising interest rates can increase the overall cost of borrowing, meaning students might pay more over the life of their loans. This could influence decisions about how much to borrow, whether to pursue certain programs, or how to manage repayment. Conversely, if rates decrease, borrowing becomes more affordable, potentially easing financial burdens.

Q6: Are there strategies borrowers can use to manage fluctuating interest rates?

A6: Borrowers can consider consolidating or refinancing loans to lock in lower rates, especially if market conditions become favorable. Staying informed about rate changes and budgeting carefully can also help manage repayment effectively. For federal loans, income-driven repayment plans and forgiveness programs might provide additional relief.

Q7: How can students stay updated on interest rate changes?

A7: Monitoring official sources like the U.S. Department of Education’s Federal Student Aid website, subscribing to financial news outlets, and consulting with financial aid advisors can ensure students and borrowers stay informed about rate changes and what they mean for their loans.

This Q&A offers a clear, creative snapshot of the evolving landscape of student loan interest rates, helping readers understand what’s changing and how it might affect their financial journey.

Wrapping Up

As the landscape of student loan interest rates shifts, borrowers and prospective students alike find themselves at a crossroads of opportunity and uncertainty. Understanding these changes is more than just a financial necessity-it’s a step toward making informed decisions that will shape educational journeys and future finances. While the exact impact may unfold over time, staying informed empowers you to navigate this evolving terrain with confidence. After all, knowledge is the interest that truly compounds over a lifetime.